Introduction to Credit Scores and Their Importance

Your credit score is more than just a number—it’s a key factor that determines your financial credibility. From applying for a mortgage to getting approved for a credit card, this three-digit figure can significantly influence your ability to access financial services. Credit scores are used by lenders, landlords, and even some employers as a measure of how trustworthy and financially responsible you are. But in the process of managing your credit, a common question arises: does checking your credit score lower it? To answer this, it’s essential to understand how credit scores work, how they’re evaluated, and the type of credit checks involved.

Understanding Credit Checks: Soft vs. Hard Inquiries

To grasp how credit checks impact your credit score, you first need to know the difference between soft inquiries and hard inquiries. Credit checks—or inquiries—are records that indicate someone has reviewed your credit report. When a lender or company evaluates your creditworthiness, your credit file is accessed through one of these two methods.

Soft inquiries are typically non-threatening because they occur when you check your own credit score or when companies pre-approve you for financial products. On the other hand, hard inquiries are made by lenders during formal applications for financial products like loans, credit cards, or mortgages. Since hard inquiries signal active borrowing intentions, they carry more weight and may affect your credit score. Understanding these differences is key to knowing whether checking your credit score personally has any adverse effects.

The Impact of Soft Inquiries on Your Credit Score

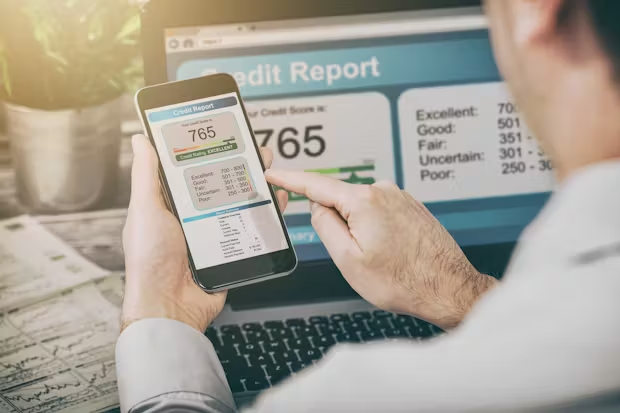

If you’ve hesitated to check your credit score out of fear of lowering it, here’s some good news—soft inquiries do not impact your credit score. When you check your own credit through services like annualcreditreport.com or apps offered by your bank, it creates what’s called a “soft pull.”

Soft inquiries provide a snapshot of your credit without being visible to lenders. They’re solely for you, empowering you to monitor your financial health without any negative consequences. Whether you’re checking your credit score monthly or just before making key financial plans, soft inquiries ensure there’s zero risk of damaging your credit. This dispels the myth that keeping track of your score on a regular basis is harmful.

When Hard Inquiries Affect Your Credit Score

Unlike soft inquiries, hard inquiries can slightly affect your credit score, but only under specific circumstances. A hard inquiry happens when a lender or financial institution performs a deep check of your credit during an application for a financial product. Since such inquiries signal that you’re actively looking for credit, they may temporarily lower your score by a few points.

However, the impact of hard inquiries is minimal and short-lived. For example, a single hard inquiry usually lowers your score by less than five points and disappears from your credit report in about two years. But frequent applications, resulting in many hard inquiries within a short time frame, might signal financial distress, flagging potential concerns for lenders. It’s a good practice to avoid multiple applications close together unless necessary.

Common Misconceptions About Checking Your Credit Score

One of the biggest misconceptions in personal finance is the belief that checking your credit score automatically lowers it. This myth likely stems from confusion between soft and hard inquiries. Many consumers mistakenly think that any inquiry—even if it’s initiated by the individual—could tank their score.

Another common misunderstanding is that inquiries of any kind have the same impact. While hard inquiries made during credit applications are more significant, they still don’t create drastic changes in your credit score, contrary to popular belief. These misconceptions often lead to people neglecting proper credit monitoring, weakening their ability to detect errors or signs of identity theft early.

Best Practices for Monitoring Your Credit Score

If monitoring your credit score doesn’t lower it, how often should you check it? The answer depends on your financial habits and goals. Generally, it’s a good idea to review your credit at least once a year through free, authorized services such as Annual Credit Report. For a more proactive approach, consider subscribing to credit monitoring tools that provide monthly updates and alert you to any changes.

These services also help by identifying potential inaccuracies in your credit report that could unfairly affect your score. Regularly monitoring your credit ensures you’re prepared to correct mistakes quickly, resolve disputes, and maintain control over your financial profile. By staying informed without fear of consequences, you’re safeguarding your financial future.

Debunking the Myth and Empowering Credit Management

To wrap things up, checking your credit score does not lower it when done responsibly. Soft inquiries—those initiated by you for your personal reference—have zero impact. Hard inquiries may result in a small, temporary dip, but only when associated with formal financial applications.

Understanding the nuances of credit checks allows you to debunk widespread myths while confidently managing your credit health. Knowledge is power, and staying engaged with your financial data keeps both your credit score and long-term goals on track. The next time you think twice about checking your score, remember it’s a harmless step that could save you from financial surprises.

FAQ

Does checking my credit score through apps affect my rating?

No, apps like Credit Karma and Experian perform soft inquiries that won’t impact your credit score.

How often should I check my credit score?

Checking your score once a month or quarterly is ideal for tracking progress while ensuring your financial health stays intact.

Can multiple hard inquiries ruin my credit?

Not necessarily. While multiple hard inquiries within a short period can temporarily lower your score, they don’t have a significant long-term impact.

Why is monitoring my credit score important?

Regular monitoring helps you detect errors, signs of identity theft, and areas for financial improvement—key steps to building a solid credit history.